Where Is Smart Money Moving in 2026? 5 Sectors FIIs Are Betting On

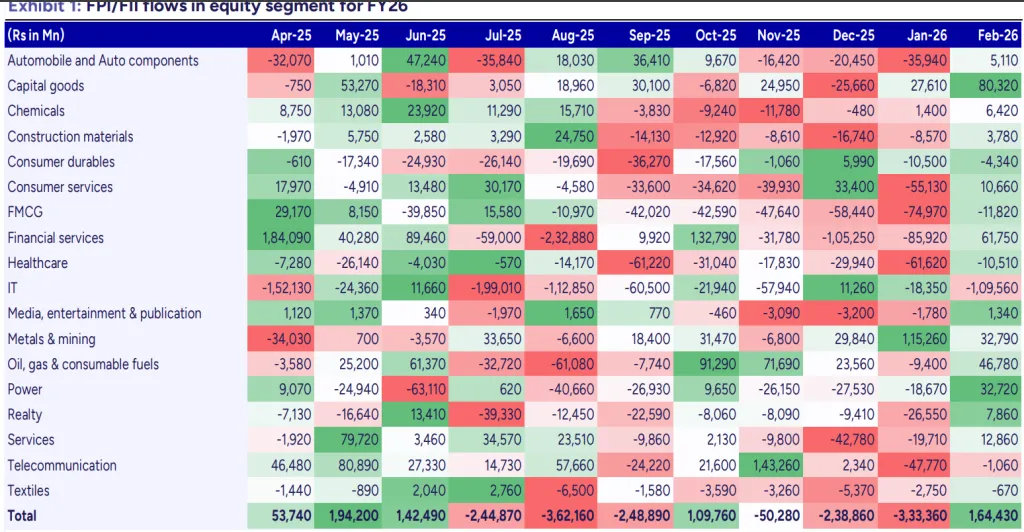

If you've been tracking Indian markets in early 2026, you already know the mood swings have been brutal. January 2026 saw foreign institutional investors (FIIs) and foreign portfolio investors (FPIs) pull out a massive Rs33,336 crore from Indian equities across sectors. Then February came along and flipped the script almost entirely — total inflows hit Rs16,443 crore.

That is not a small bounce. That is a significant reversal in sentiment, and it happened fast.

According to data from PL Capital's Quant research team, 12 out of 18 sectors tracked turned positive in February 2026, compared to just three sectors that managed to attract foreign money in January. So where exactly is this money going? And which sectors are still being dumped? Let's break it down in plain language.

The 5 Sectors Where Smart Money Is Flowing In

1. Capital Goods — The Biggest Winner

Capital Goods was the clear standout performer in February 2026, attracting FII/FPI inflows of Rs8,032 crore. To put that in perspective, the long-term average monthly inflow for this sector is Rs 1,966 crore — meaning February's number was roughly four times the historical norm. This sector includes companies involved in industrial machinery, defense equipment, power equipment, and infrastructure-related manufacturing. The strong buying here signals that foreign investors are betting on India's continued push toward manufacturing and infrastructure development.

Interestingly, the sector had seen outflows of Rs 4,464 crore in February 2025, so this is a complete turnaround compared to the same time last year.

2. Oil, Gas & Consumable Fuels — A Sharp Comeback

After outflows in both February 2025 (Rs 3,377 crore) and January 2026 (Rs 940 crore), the Oil & Gas sector saw a dramatic reversal with inflows of Rs 4,678 crore in February 2026. This is significantly better than its long-term average, which actually shows an average outflow of Rs 1,814 crore.

In other words, foreign investors not only stopped selling this sector — they bought it at a level that beats its historical trend by a wide margin. Energy sector reforms, crude oil pricing dynamics, and India's growing domestic consumption story may all be factors driving renewed interest.

3. Financial Services — Confidence Returns

Financial Services had been one of the hardest hit sectors in recent months. It saw outflows of Rs 8,592 crore in January 2026 alone, on top of outflows of Rs 6,991 crore in February 2025. That's a lot of money leaving the sector over a sustained period.

February 2026 brought a sharp reversal with inflows of Rs 6,175 crore. While this is still not fully back to historical highs, it is a meaningful signal that confidence is returning to India's banking, insurance, and financial services space. Given that Financial Services is one of the largest components of the Indian equity market, its recovery matters a great deal for overall market health.

4. Metals & Mining — Momentum Continues

Metals & Mining had already seen massive buying in January 2026 (Rs 11,526 crore), and that momentum continued into February with inflows of Rs 3,279 crore. The long-term average for this sector is just Rs 212 crore, so even February's moderated inflow is well above historical norms.

Global commodity cycles, China's demand outlook, and India's domestic steel and mining growth story are likely keeping foreign investors interested here.

5. Power — Reversing a Long Losing Streak

The Power sector had been seeing consistent outflows for several months — Rs 3,086 crore in February 2025, and Rs 1,867 crore in January 2026. February 2026 brought a meaningful turnaround with inflows of Rs 3,272 crore.

The sector's long-term average actually shows an outflow of Rs622 crore, so February's buying was notably strong against both recent trends and historical patterns. India's massive push toward renewable energy, grid expansion, and electricity demand from new industries is making this sector increasingly attractive to global investors.

Sectors That Also Turned Positive

Beyond the top five, several other sectors saw money return in February 2026 after difficult months. Consumer Services flipped from Rs5,513 crore in outflows in January to Rs1,066 crore in inflows in February. Realty similarly reversed from Rs 2,655 crore in outflows to Rs 786 crore in inflows. The Services sector and the Chemicals sector also stayed in positive territory.

However, most of these sectors are still running below their long-term averages, meaning foreign investors have returned but are not yet buying in full conviction.

The Sectors Still in the Red

Not every sector joined the party in February. Some sectors remained in outflow territory, and one of them is a major concern.

Information Technology (IT) was by far the biggest drag on the overall picture. Outflows hit Rs 10,956 crore in February 2026, far worse than January's Rs 1,835 crore outflow, and dramatically worse than the long-term average outflow of Rs 2,613 crore. IT had actually seen inflows of Rs 805 crore in February 2025, making this year's reading a sharp negative surprise.

Concerns around US discretionary spending, global tech slowdown narratives, and potentially stretched valuations in Indian IT stocks appear to be driving this sustained selling pressure. Until this reverses, it will remain a significant headwind for the broader market.

Healthcare also stayed negative with outflows of Rs 1,051 crore in February, even though that was a sharp improvement from Rs 6,162 crore in outflows the previous month. The sector's long-term average is actually an inflow of Rs 534 crore, so it remains well below where it should be.

FMCG continued to bleed with Rs 1,182 crore in outflows, though that was a big improvement from Rs 7,497 crore in January. FMCG has now seen sustained selling for several months as foreign investors appear to be rotating away from defensive consumer staples.

Consumer Durables saw outflows of Rs 434 crore in February, broadly in line with its long-term average outflow of Rs 547 crore. Not alarming, but not recovering either.

Telecommunication also remained in outflow territory at Rs 106 crore, despite having seen Rs 7,998 crore in inflows as recently as February 2025. Telecom has been on a declining trajectory and remains well below its long-term average inflow of Rs 1,635 crore.

What Does This All Mean?

The February 2026 data tells a clear story: foreign investors are coming back to India, but they are being very selective about where they put their money.

The sectors attracting the most love share a common theme — they are tied to India's physical economy. Capital Goods, Power, Oil & Gas, Metals & Mining, and Financial Services are all sectors that benefit from infrastructure spending, industrial growth, and economic expansion. Foreign investors appear to believe in India's long-term growth story, especially as it relates to manufacturing, energy, and investment-led sectors.

On the other hand, sectors that are more exposed to global technology spending (IT), defensive consumption (FMCG), or are premium-valued (Consumer Durables) are continuing to face selling pressure. This reflects a global theme where investors are rotating from growth-at-any-price assets toward sectors with clearer near-term earnings visibility.

The IT sector's massive outflows deserve special attention. India's IT index is a significant part of the market, and if that bleeding continues, it could offset a lot of the good news coming from other sectors.

The Bottom Line

February 2026 was a good month for India's FII/FPI flows — no question. The swing from Rs 33,336 crore in outflows in January to Rs 16,443 crore in inflows in February 2026 is a strong signal that global investors have not given up on India.

But the recovery is uneven. If you're watching where the smart money is moving, the clearest answer right now is: infrastructure, energy, metals, and financials are in favor. Technology and defensives are not.

The global backdrop adds another layer of complexity to this picture. With the Russia-Ukraine war still unresolved and ceasefire negotiations remaining fragile, energy supply chains across Europe continue to stay under pressure, which partly explains why global investors are warming up to India's Oil & Gas sector as an alternative bet. Meanwhile, rising tensions between the US and Iran in the Middle East are keeping crude oil prices on edge, making energy-linked equities globally more attractive.

On the metals front, the ongoing geopolitical realignment, with Western nations actively seeking to reduce dependence on Russian and Chinese supply chains, is pushing investors toward markets like India that can benefit from this shift in global commodity flows. Even the Capital Goods rally makes more sense in this context: as countries race to rearm, rebuild, and restructure their supply chains away from conflict zones, India's manufacturing ambitions are looking increasingly well-timed.

As always, past flows are not a guarantee of future direction — but when you see Rs8,032 crore pouring into Capital Goods or Rs4,678 crore moving into Oil & Gas in a single month, and you layer that on top of a world that is actively repricing geopolitical risk, that is a data point very much worth paying attention to.