High PE Stocks: Bubble or Opportunity? Here's How to Tell the Difference

If you have spent any time reading about Indian stocks, you have probably come across the term "PE ratio" — usually followed by either excitement ("this stock is available at just 12x!") or alarm ("this stock is trading at 150x, it's a bubble!"). But very few articles actually explain what PE means, why it matters, and — most importantly, why a high PE is sometimes a gift and sometimes a trap. This article breaks it all down, with a real Indian stock example to make it concrete.

What Exactly Is the P/E ratio?

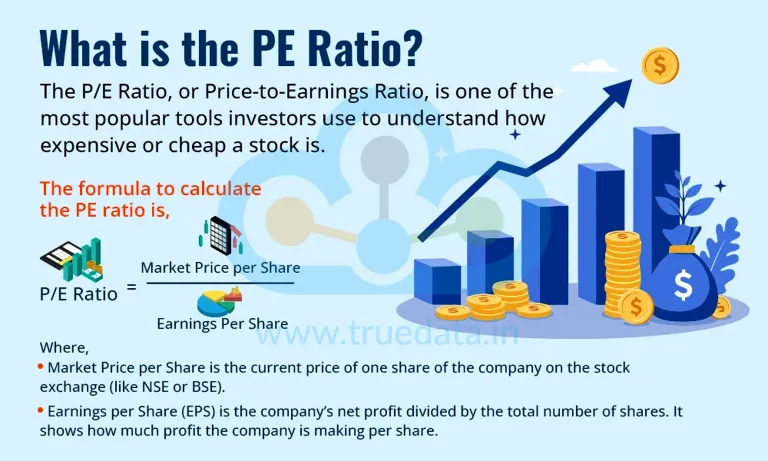

PE stands for Price-to-Earnings ratio. The formula is straightforward:

PE Ratio = Stock Price ÷ Earnings Per Share (EPS)

Or alternatively:

PE Ratio = Market Capitalisation ÷ Net Profit

Both give the same result. In plain English, the PE ratio tells you how many rupees investors are willing to pay for every ₹1 of profit the company earns. If a company has a PE ratio of 25, investors are willing to pay ₹25 for each rupee of the company's current earnings, essentially valuing the stock at 25 times its current earnings, with an expectation of future growth built in.

So if a company earns ₹10 per share and trades at ₹300, its PE is 30. If it trades at ₹1,000 for the same ₹10 in earnings, the PE is 100. The higher the PE, the more expensive the stock is relative to what it currently earns, and the more growth investors are betting on.

Why Does PE Even Matter?

Think of PE as a price tag on future expectations, not just current reality. When you buy a stock, you are not buying yesterday's profits, you are buying a stake in all the profits this company will earn in the future. A high PE simply means the market believes those future profits will be much larger than they are today. A low PE means the market either thinks growth will be slow or it is uncertain whether the business will survive at all.

Neither is automatically good or bad. Context is everything.

When a Low PE Is Good and When It's a Warning Sign

A low PE, generally anything below 15 in the Indian context, though this varies by sector, can be a sign of genuine undervaluation. Undervalued stocks are identified using key financial metrics such as the P/E ratio, price-to-book ratio, return on equity, and historical growth trends, indicators that help assess whether a stock is priced below its intrinsic value relative to its financial performance.

If a fundamentally strong company with growing revenues and healthy margins is trading at a low PE simply because the broader market has sold off, that can be a genuine buying opportunity. Value investors, followers of the Warren Buffett school of investing, actively hunt for these situations.

But a low PE is not always good news. It can also signal deep problems: a business facing structural decline, an industry being disrupted, or a company carrying enormous debt that will eventually eat into profits. While low valuation metrics may indicate potential value, investors should consider sector-specific risks and cyclical factors — industries such as automotive and shipping are sensitive to economic cycles, which can impact earnings stability.

In short: a low PE on a great business is a bargain. A low PE on a struggling business is a value trap as the stock looks cheap, but it is cheap for a very good reason.

When a High PE Is Justified and When It's Dangerous

A high PE, anything above 40–50 on the Indian market is considered elevated, though some sectors routinely trade above 80–100, typically reflects one of two things: either the market genuinely expects the company's earnings to grow very rapidly in coming years, or it has simply gotten swept up in hype and momentum with no earnings to back it up.

The key distinction is growth. If a company is currently earning ₹100 crore but is credibly expected to earn ₹500 crore in three years, because it has new product lines, a massive order book, government contracts, or a structural market tailwind, then paying 80x today's earnings may actually be cheap relative to tomorrow's earnings. This is called "growth investing," and it has created enormous wealth in Indian markets over the past decade in sectors like defence, electronics manufacturing, and quick commerce.

The danger emerges when the high PE is built on hope, narrative, and momentum alone, with no credible path to earnings catching up to the price. A good number of large defence PSUs have been trading at 40x–60x PE multiples with full order books for the next five years, but with limited execution capacity, and when the market is valuing a "Super Budget" scenario but receives a "Normal Budget," high-PE stocks plummet. Expectations built into a high PE are fragile. When reality disappoints, even slightly, the re-rating can be brutal and swift.

Real Examples

No Indian stock illustrates the high-PE debate more vividly than Dixon Technologies, the country's largest contract electronics manufacturer.

For much of 2024 and into early 2025, Dixon was trading at a PE of over 120 times earnings, a number that, in isolation, looks staggering. Dixon was considered expensive and overvalued with a PE ratio of 122.81, significantly higher than industry peers, despite delivering a strong return of 48.63% over the prior year. The question investors faced was the classic high-PE dilemma: Is this justified, or is this a bubble about to burst?

The bull case was specific and evidence-backed. Dixon was growing revenues at 65–70% in FY26 and had entered Apple's iPhone manufacturing supply chain, a transformative corporate event that could see it producing sub-assemblies for 25–30% of iPhones made in India by FY27. Analyst targets ranged from ₹16,000 to ₹20,000, with firms including Nuvama, ICICI Securities, and JM Financial backing the thesis. The argument was not that Dixon was cheap at 120x PE, it was that the PE would compress rapidly as earnings grew to match the price. In the jargon, investors were betting on "PE re-rating driven by earnings growth."

By early 2026, that compression had indeed occurred. Dixon's PE had fallen to approximately 43 times earnings, near a five-year low of 43, reflecting exactly what growth investors hoped for: profits catching up with the share price. Those who bought at the "alarmingly high" 120x PE and held through the earnings growth cycle were rewarded. Those who saw only the headline PE and stayed away missed one of the decade's stronger manufacturing stories.

But Dixon also illustrates the risk. The stock is a high-conviction growth bet, not a value play, and the risk-reward depends entirely on execution. If the Apple ramp materialises as projected, current valuations will appear reasonable in hindsight. If execution stumbles, delayed orders, PLI disbursement issues, loss of the Apple contract, the same high PE that looked justified would suddenly look like a classic bubble. GuruFocus currently classifies Dixon as a "Possible Value Trap," noting its GF Value at roughly ₹22,069 against a price of around ₹10,263. The debate is very much alive.

The Analyst Divide: What the Experts Say

Analysts are rarely unanimous on high-PE stocks, and for good reason — the answer genuinely depends on your assumptions about the future.

On the cautious side, Siddhartha Bhaiya of Aequitas Investment Consultancy has characterised large pockets of the Indian market as overvalued on a PE basis, noting that prices have run far ahead of earnings in several sectors. The concern is not that Indian businesses are bad — it is that the future has been priced in too aggressively, leaving little room for error.

Taking the opposite view, Deven Choksey of DRChoksey FinServ has argued that high valuations in sectors with clear earnings visibility should be understood as reflective of long-term opportunity rather than near-term excess. His argument: if you are investing for ten years, paying 60x today's earnings for a company whose earnings will be 10x larger in a decade is not expensive, it is rational.

Sandip Sabharwal's view threads a middle path: the overall market is not in a bubble, but specific pockets, particularly certain defence and capital goods names, have been priced for perfection. Investors are advised to focus on fundamentally strong stocks and avoid abnormally priced, story-driven narratives.

Motilal Oswal's framework is perhaps the most practical for retail investors. Their QGLP model (Quality, Growth, Longevity, Price) explicitly includes price as one of four filters, a reminder that even a great business can be a bad investment if you pay too much for it. Even if you find a great stock, how you invest matters as much as what you buy, and even a great company can be a bad investment if you buy it when the price is too high.

The One Question That Settles the Debate

When confronted with a high-PE stock, the single most important question to ask is not "Is this PE high?" It is "will earnings grow fast enough to justify this PE, and do I have genuine evidence for that, not just hope?"

A PE of 80 on a company growing profits at 50% per year will compress to a PE of 35 in just two years if the growth holds. A PE of 80 on a company growing profits at 5% per year will still be 80 in two years and likely much lower if the market finally loses patience.

The formula is simple: Future PE = Current Price ÷ Future EPS. Model out what earnings look like two to three years from now under realistic — not optimistic — assumptions. If the implied future PE is reasonable, the current high PE may be justified. If even aggressive assumptions leave the future PE elevated, you are paying for a story, not a business.

In Indian markets today, with the Nifty's trailing PE having fallen below 20 times after the recent correction, the conversation around valuation has become more nuanced. The era of "growth at any price" that characterised the 2021–2024 bull run is over, at least temporarily. What remains is an opportunity to distinguish between high-PE stocks that are genuinely pricing in superior growth and those that are simply expensive. One is a potential opportunity. The other is a bubble in slow motion.

Knowing the difference is the whole game.