US Interest Rates Explained: Why Indian Markets Care A Complete Guide

01. The Most Powerful Number in the World

Every few weeks, a committee of twelve people meets in Washington, D.C. They do not command armies, control oil fields, or run any company. They sit around a table, review economic data, and vote on a number — typically expressed in fractions of a percentage point.

Yet when that number moves, stock markets from Tokyo to São Paulo flinch. The Indian rupee shifts. Gold prices react. Loan rates in Chennai and Coimbatore may change in the months that follow. Commodities priced in dollars — including the crude oil that powers 85% of India's energy needs — get repriced overnight.

That number is the US Federal Funds Rate. And understanding it is not just an academic exercise for economists. For every Indian investor, business owner, and working professional, it is one of the most consequential forces shaping their financial lives — whether they know it or not.

This is the complete guide to understanding it.

02. What Is the US Interest Rate — and Who Sets It?

The Federal Reserve — commonly called "the Fed" — is the central bank of the United States. It was established in 1913 to provide the country with a safer, more flexible monetary and financial system. Today, it is arguably the most powerful financial institution on earth.

The Fed's primary lever is the Federal Funds Rate — the interest rate at which American banks lend money to each other overnight. Think of it as the "base price of money" in the US economy. When the Fed raises this rate, borrowing becomes more expensive across the entire economy. When it cuts the rate, credit becomes cheaper and easier to access.

This rate is set by the Federal Open Market Committee (FOMC) — a 12-member body that meets eight times a year. Each meeting ends with a policy statement and, if warranted, a change in the rate.

Hawkish vs. Dovish: Two Words Every Investor Must Know

The Fed communicates its future intentions through language that market participants parse obsessively:

Hawkish = the Fed signals it is inclined to raise rates. Fighting inflation is the priority, even at the cost of slower growth.

Dovish = the Fed signals it may cut rates or keep them low. Stimulating growth and employment is the priority.

A single word in the FOMC statement can move global markets by billions of dollars within seconds. That is how closely watched this institution is.

As of early 2025, the Federal Reserve had maintained its benchmark rate in the range of 4.25%–4.50% — a historically elevated level — after an aggressive hiking cycle intended to bring US inflation back to its 2% target.

03. How Interest Rates Work: Bonds, Mortgages & Household Debt

Before exploring the global domino effect, it helps to understand how interest rates transmit through an economy — starting with the US itself.

Bonds: The Heartbeat of the Financial System

A bond is simply a loan. When you buy a government bond, you are lending money to the government in exchange for regular interest payments (called the "coupon") and the return of your principal at maturity. The price of a bond and its yield (effective interest rate) move in opposite directions — when yields rise, bond prices fall, and vice versa.

When the Fed raises rates, newly issued US government bonds offer higher yields. This makes existing bonds (with lower yields) less attractive, pushing their prices down. More importantly, rising bond yields ripple through the entire financial system because bonds are the benchmark against which every other asset is priced.

The US 10-Year Treasury: The World's Risk-Free Rate

The yield on the 10-year US Treasury bond is perhaps the single most important financial price on the planet. It serves as the "risk-free rate" — the baseline return an investor can earn with no credit risk. Every other investment — stocks, corporate bonds, real estate, emerging market debt — must justify itself by offering a return above this baseline.

When the 10-year yield rises significantly, money gravitates toward it. It is safe, liquid, and now generously rewarding. The ripple effects reach every corner of the globe.

Mortgages and Household Debt

In the US, most home loan rates are closely tied to the 10-year Treasury yield. When the Fed raises rates:

Mortgage rates rise (the 30-year fixed mortgage rate crossed 7–8% in 2023–24, levels not seen since the early 2000s)

Car loan rates rise

Credit card interest rates rise

Corporate borrowing costs rise

American consumers and businesses feel the squeeze almost immediately. Spending slows. Housing markets cool. Corporate investment decisions get postponed. The economy slows — which is often exactly what the Fed intends when fighting inflation.

When the Fed cuts rates, the opposite occurs. Credit becomes cheaper. Spending rises. Confidence returns. The economy accelerates.

Now here is the critical insight: what happens in the US economy does not stay in the US economy. Through several powerful transmission channels, these changes radiate outward — and India sits directly in their path.

04. Dollar Supremacy: How America's Currency Became the World's Currency

To understand why US interest rates matter globally, you must first understand why the US dollar rules the world.

The Bretton Woods Foundation

In July 1944, with World War II still raging, delegates from 44 Allied nations gathered at a resort in Bretton Woods, New Hampshire. They needed to design a new post-war global financial system. The agreement they reached established the US dollar as the world's primary reserve currency, pegged to gold at $35 per ounce. All other currencies were pegged to the dollar.

The logic was straightforward: the US had emerged from the war as the dominant industrial and military power, holding two-thirds of the world's gold reserves. The dollar was the most stable, most trusted currency on earth.

In 1971, President Nixon ended the dollar's direct convertibility to gold — known as "closing the gold window." The Bretton Woods peg collapsed. But the dollar's dominance did not. Something else replaced the gold peg and cemented the greenback's supremacy for the next five decades: oil.

Dollar Dominance Today

The dollar's status as the world's reserve currency gives the United States what former French Finance Minister Valéry Giscard d'Estaing famously called an "exorbitant privilege" — the ability to borrow money at lower interest rates than any other nation, simply because the entire world needs dollars to conduct trade.

Today, roughly 60% of global central bank reserves are held in US dollars. Approximately 90% of all foreign exchange transactions involve the dollar on one side. It is the default currency for international trade, commodity pricing, and financial contracts.

When the Fed changes its rates, it changes the value of this globally dominant currency — and that change affects every country that saves in dollars, trades in dollars, or has borrowed in dollars.

05. The Petrodollar: Why Crude Oil Flows Through the Dollar

No story of dollar supremacy is complete without understanding the petrodollar — one of the most consequential and least discussed arrangements in modern economic history.

The 1974 Deal That Wired the World

After Nixon ended the gold standard in 1971, the dollar lost its material backing. Henry Kissinger, then National Security Advisor, negotiated a secret agreement with Saudi Arabia in 1974: Saudi Arabia would price its oil exclusively in US dollars, and would reinvest its oil revenues (called "petrodollars") into US Treasury bonds. In exchange, the United States would guarantee Saudi Arabia's security — through military presence, arms sales, and protection of Gulf shipping lanes.

Other OPEC nations followed. The deal was struck.

The genius of this arrangement was the self-reinforcing loop it created: because oil is priced in dollars, every nation that needs oil — which is every nation — needs dollars. China must acquire dollars to buy Saudi crude. India must hold dollars to pay for Iranian oil. Japan must keep dollar reserves to fund its energy imports. This creates permanent, structural global demand for the dollar, independent of US economic performance.

What This Means in Practice

India imports approximately 80–85% of its crude oil requirements. Every barrel of that oil — regardless of whether it comes from Saudi Arabia, Iraq, UAE, Russia, or the US — is priced and settled in US dollars. When the dollar strengthens (often a consequence of rising US interest rates), India's oil import bill rises automatically, even if the dollar price of oil itself hasn't changed.

This creates a direct, unavoidable link between US monetary policy and India's energy costs, trade deficit, and inflation.

The System Today: Cracks Appearing

The petrodollar system, while still dominant, is facing its most serious challenge in decades. Saudi Arabia quietly allowed its 50-year petrodollar agreement with the US to expire in mid-2024 without renewal. China has been actively pursuing yuan-denominated oil contracts. Russia — after Western sanctions following the Ukraine invasion — pivoted much of its energy trade to yuan and rupee settlements. As of early 2025, an estimated 20–25% of China's oil imports were settled in currencies other than the dollar, up from near zero a decade earlier.

However, the dollar remains structurally dominant. Over 80% of global oil transactions are still denominated in dollars. Any transition away from petrodollar dominance, if it comes, will be gradual — but for India, which has already experimented with rupee-settled oil trade with Russia, the shifts are worth watching closely.

06. The Transmission Mechanism: How a Rate Change in Washington Reaches Mumbai

When the Fed raises or cuts rates, the impact on India does not arrive via a single channel. It travels through multiple interconnected pipelines simultaneously.

Pipeline 1: The Dollar Strengthens or Weakens

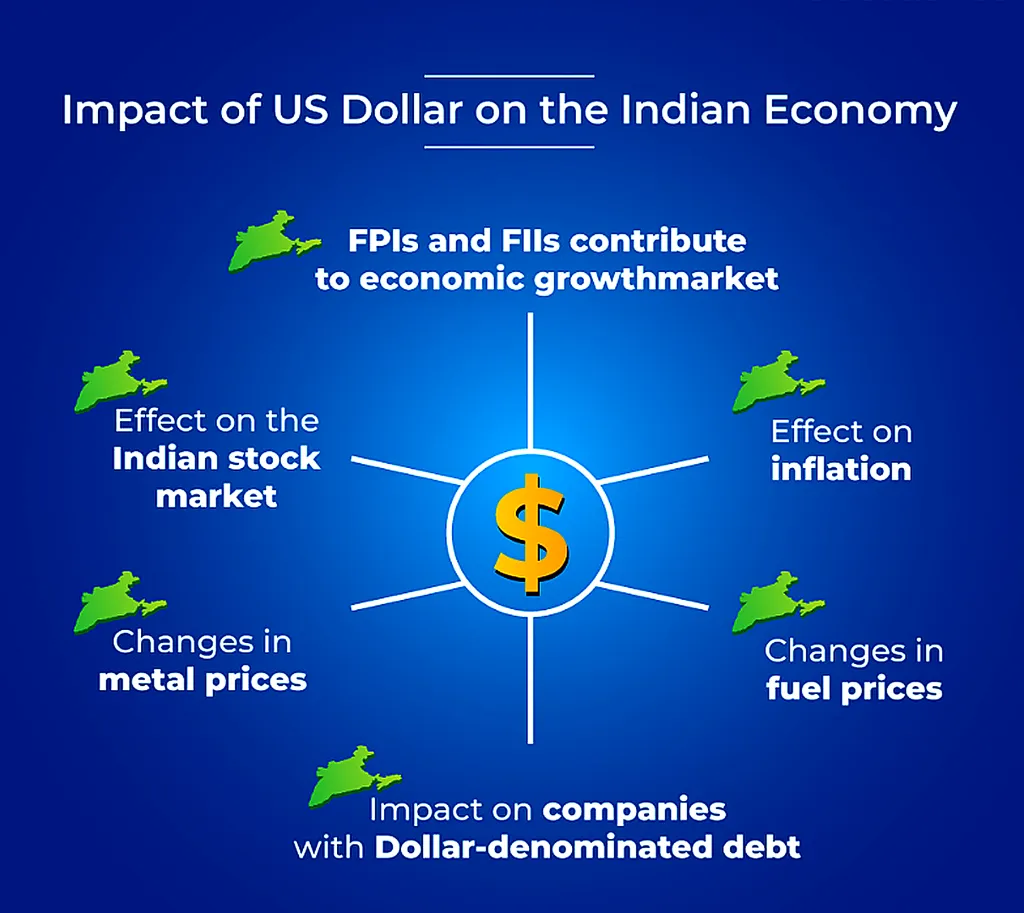

Rising US interest rates attract capital from around the world toward US assets — particularly US Treasuries offering higher yields. As global investors buy dollars to purchase these assets, demand for the dollar surges. The dollar strengthens against most currencies, including the Indian rupee. A stronger dollar means:

Indian imports (especially oil, electronics, capital goods) become more expensive in rupee terms

India's foreign debt burden rises (debt denominated in dollars becomes costlier to repay)

Imported inflation filters into the Indian economy

Pipeline 2: Capital Flows Migrate

When the US offers, say, 5% risk-free returns on Treasuries, global investors reassess: "Why should I take the risk of Indian equities or bonds when I can earn 5% safely from the world's most liquid market?" This triggers capital outflows from India — Foreign Portfolio Investors (FPIs) sell Indian stocks and bonds, repatriating money to the US. This selling pressure pushes Indian equity markets lower and the rupee weaker.

Pipeline 3: Commodity Prices Re-Priced

Most global commodities — crude oil, gold, copper, coal, natural gas — are priced in dollars. A stronger dollar (caused by higher US rates) typically suppresses commodity prices in dollar terms (since non-US buyers can afford less). However, for a country like India, even if crude falls slightly in dollar terms, a depreciating rupee can mean the rupee cost of that crude actually rises.

Pipeline 4: RBI's Constrained Choices

The Reserve Bank of India operates in the shadow of Fed policy. If the Fed raises rates aggressively and the RBI doesn't respond, the interest rate differential between the two countries narrows. This makes Indian assets less attractive to foreign investors, worsening capital outflows and rupee weakness. The RBI is therefore often compelled to mirror Fed moves — even if India's domestic inflation and growth conditions don't require it.

07. The Capital Flow Seesaw: When Money Migrates

Perhaps the most visceral channel through which US rates affect India is through capital flows — the movement of investment money across borders.

Global financial markets operate on a simple principle: capital moves toward the best risk-adjusted return. When US interest rates are low (as they were from 2008 to 2022), US Treasuries offered paltry returns of 1–2%. In that environment, professional investors — pension funds, hedge funds, sovereign wealth funds — looked elsewhere for yield. Emerging markets like India, offering higher growth rates and higher interest rates, became magnets for this capital.

The results were dramatic. In FY2021, Foreign Portfolio Investors pumped a record ₹2.74 trillion (approximately $37 billion) into Indian markets — the best annual foreign inflow in over a decade. The Sensex and Nifty delivered stunning returns. Indian unicorns attracted billions in venture capital. The rupee stayed relatively strong.

Then, in 2022, the Fed began its most aggressive rate-hiking cycle in four decades — raising rates from near zero to over 5% in just 18 months. The calculus flipped. Suddenly, a risk-free 5% return in the world's safest market was available. The same FPIs that had flooded into India began withdrawing. In 2022, FPIs pulled out over ₹1.2 lakh crore from Indian equities — one of the largest outflows on record. The Sensex dropped significantly. The rupee fell toward 83 against the dollar.

This is the capital flow seesaw: when US rates rise, the seesaw tilts away from India; when US rates fall, it tilts toward India. The scale of these movements — billions of dollars shifting within weeks — means that Indian market participants can never fully ignore what the Fed is doing, no matter how strong India's domestic fundamentals are.

08. The Rupee Under Pressure: Currency, Inflation & Import Costs

The Indian rupee's exchange rate against the US dollar is one of the most sensitive indicators of how India is faring in the global capital flow seesaw.

How US Rates Weaken the Rupee

When US rates rise and capital flows out of India, foreign investors sell their Indian assets (stocks, bonds) and convert the rupee proceeds back into dollars. This surge in dollar demand — and rupee selling — weakens the rupee. The mechanism is straightforward: more people want dollars, fewer want rupees, so the rupee's price falls.

The rupee has shown a long-term depreciating trend against the dollar — from around ₹45/$ in 2000 to ₹83–87/$ in 2024–25. While structural factors (India's current account deficit, inflation differential) explain much of this, US rate cycles play a significant amplifying role.

Why a Weaker Rupee Is Painful for India

India is structurally a net importer. The country imports crude oil worth $130–150 billion annually, electronics worth over $70 billion, and significant quantities of gold, fertilisers, machinery, and defence equipment. Almost all of this is priced in dollars.

When the rupee weakens by just ₹1 against the dollar:

India's annual oil import bill rises by approximately ₹8,000–10,000 crore

Companies with dollar-denominated borrowings face higher repayment costs

Airlines (which pay for fuel in dollars) see costs surge

Electronics and appliances become more expensive for consumers

This imported inflation is a direct consequence of a weaker rupee — which is often a direct consequence of US rate hikes. The chain runs from a Fed meeting room in Washington to the price of petrol at a pump in Pune.

When the Rupee Strengthens: A Double-Edged Sword

Rate cuts from the Fed can cause the dollar to weaken and the rupee to appreciate. While this lowers import costs (beneficial for oil and electronics importers), it creates a different challenge: it makes Indian exports more expensive for foreign buyers. India's IT services sector, textiles, pharmaceuticals, and manufacturing exporters earn revenues in dollars. A stronger rupee means those dollar revenues convert to fewer rupees — compressing margins and earnings.

09. Impact on Indian Bonds and RBI's Balancing Act

The Bond Market Connection

The Indian government bond market — totalling over ₹100 lakh crore — is deeply influenced by US rate decisions. Here is how:

When US Treasury yields rise (a consequence of Fed rate hikes), global bond investors demand higher yields on Indian bonds too. After all, if a "safe" US bond pays 5%, why would an investor accept 6.5% on a "riskier" Indian government bond? The premium demanded for taking India risk (currency risk, political risk, economic uncertainty) has to widen. This pushes Indian bond prices down and yields up.

Higher Indian bond yields mean higher borrowing costs for the Indian government, Indian corporations, and ultimately Indian consumers. Home loan rates, business loan rates, and corporate bond rates are all influenced — directly or indirectly — by this chain.

The RBI's Impossible Triangle

The Reserve Bank of India faces what economists call the "impossible trinity" — the impossibility of simultaneously maintaining a fixed exchange rate, free capital movement, and an independent monetary policy. India operates with a managed float exchange rate and relatively open capital account, meaning the RBI has only partial independence from Fed policy.

When the Fed raises rates aggressively, the RBI faces pressure to follow — even if India's domestic economic conditions don't call for tighter money. If the RBI doesn't raise rates, the interest rate differential between India and the US narrows, capital flows out, and the rupee weakens. If the RBI does raise rates to defend the currency, it slows domestic growth and squeezes borrowers.

This dilemma played out vividly in 2022–23, when the RBI raised its repo rate by 250 basis points in step with the Fed cycle — even as Indian inflation, though elevated, was driven more by food prices than by demand-side excess that higher rates could address.

Conversely, when the Fed cut rates by 50 basis points in September 2024 — its first cut in four years — it gave the RBI the breathing room it needed. India's central bank followed with rate cuts in early 2025, allowing domestic borrowing costs to ease and stimulating credit growth.

10. Sector-by-Sector Impact on Indian Markets

US rate decisions do not impact all sectors equally. Here is how different parts of the Indian economy respond:

Information Technology (IT) & Software Services

India's IT sector — Infosys, TCS, Wipro, HCL — earns the majority of its revenues in US dollars from American clients. When US rates are high and the dollar is strong, these companies benefit from favourable conversion rates — the same dollar revenues translate into more rupees. However, high US rates also signal economic slowdown in America, which can lead US companies to cut technology spending budgets, directly hurting Indian IT firms' order books. The net effect is mixed and depends on whether the rate cycle is in its early or late stages.

Banking and Financial Services

Indian banks and NBFCs are significantly impacted. When US rates rise, foreign capital flowing into Indian bonds and equity falls — reducing liquidity in the system. Higher rupee bond yields raise the cost of funds for banks. When US rates fall, the reverse occurs: capital flows in, liquidity improves, and the RBI gains room to lower the repo rate — which expands bank margins on new loans and boosts credit growth.

Oil & Gas / Energy

India imports approximately 85% of its crude oil. The sector is hit from two sides during a US rate hike cycle: a stronger dollar raises the rupee cost of every barrel, and tightening global financial conditions can trigger volatility in oil prices themselves. State-owned oil marketing companies (IOC, BPCL, HPCL) bear the brunt of this through underrecoveries or pricing pressures.

Infrastructure & Real Estate

These capital-intensive sectors depend heavily on long-term debt. When US rate cycles force Indian bond yields higher and the RBI tightens policy, the cost of long-term project financing rises. Real estate developers face higher construction financing costs, and home loan EMIs for buyers increase. Rate cut cycles have the opposite, beneficial effect — and are often the trigger for real estate demand revivals.

Pharmaceuticals & Chemicals (Exporters)

Export-oriented sectors with significant US revenue actually benefit when the rupee weakens (a consequence of US rate hikes). Their dollar revenues convert to more rupees, improving profitability. Indian pharmaceutical companies, which earn a large share of their revenue from regulated US markets, are one of the few Indian sectors that can benefit from a strong dollar environment.

Gold

Gold has an interesting inverse relationship with US interest rates. When real interest rates (nominal rate minus inflation) are high, the opportunity cost of holding gold (which pays no income) rises, and gold prices fall. When the Fed cuts rates and real yields fall, gold tends to rally as investors seek stores of value. India, the world's second-largest consumer of gold, is deeply affected by these dynamics — both in terms of import costs and investment sentiment.

11. Rate Hike vs. Rate Cut: Two Scenarios for India

Scenario A: The Fed Raises Rates

The chain of events typically unfolds like this:

The Fed hikes → US Treasury yields rise → Dollar strengthens globally → Capital flows out of India as FPIs seek US yield → Rupee weakens → India's oil and import bills rise in rupee terms → Imported inflation increases → RBI faces pressure to hike rates too → Borrowing costs rise for Indian companies and consumers → Equity markets fall as earnings outlook weakens and valuations compress → Bond yields rise, pushing down bond prices.

Sectors hurt: real estate, capital-intensive manufacturing, NBFCs, auto, consumer discretionary. Sectors less affected or benefiting: IT (dollar revenue) and pharma exporters (weak rupee advantage).

Scenario B: The Fed Cuts Rates

The Fed cuts → US Treasury yields fall → Dollar weakens → Capital seeks higher returns in emerging markets → FPIs flow into India → Rupee strengthens → Oil and import costs ease → Inflation moderates → RBI gains room to cut repo rate → Borrowing costs fall → Credit growth picks up → Equity markets rally on improved liquidity, lower discount rates, and better earnings prospects.

Sectors benefiting: real estate, banking, NBFCs, auto, consumer discretionary, infrastructure. Sectors facing headwinds: IT exporters (stronger rupee erodes rupee revenues) and some commodity exporters.

The September 2024 Fed rate cut of 50 basis points set exactly this dynamic in motion for India — leading to improved FPI flows, a stronger rupee period, and eventually RBI's own easing cycle beginning in early 2025.

12. The Bigger Picture: De-Dollarisation and What It Means

No analysis of US interest rates and India would be complete without addressing the shifting tectonic plates of global finance.

The dollar's supremacy — built over eight decades — is being questioned in ways that were unimaginable a decade ago. Several forces are chipping at its foundations:

US Sanctions as a Wake-Up Call. When the US froze over $300 billion in Russian central bank reserves in 2022, nations around the world — including those not in conflict with the US — took notice. If America can effectively confiscate another country's savings, held in dollars, the "reserve currency" status of the dollar carries a hidden geopolitical risk. Countries began quietly building alternatives.

BRICS and Multipolar Finance. India, along with Brazil, Russia, China, and South Africa — and an expanding bloc of nations — has been exploring trade settlement mechanisms outside the dollar. India has already settled some oil contracts with Russia in rupees. BRICS has been discussing a common settlement platform, though a single BRICS currency remains distant.

The Petroyuan. China — the world's largest oil importer — has been steadily advancing yuan-denominated oil contracts. By 2025, an estimated 20–25% of China's oil imports settled in yuan. Saudi Arabia has shown openness to yuan payments for certain Chinese buyers. This is a direct challenge to the petrodollar system.

What This Means for India

India sits at a fascinating crossroads. It is a member of BRICS, participates in de-dollarisation discussions, and has experimented with rupee trade. Yet it remains deeply integrated into the dollar-based financial system — holding dollar reserves, borrowing in dollars, and pricing its oil imports in dollars.

A gradual de-dollarisation could, over time, reduce India's structural vulnerability to Fed policy. If India can buy oil in rupees (as it partially does with Russia), that removes the dollar transmission channel for those barrels. If India's central bank reduces its dollar reserve holdings and diversifies into other assets, it reduces exposure to dollar strengthening cycles.

However, this transition — if it comes — will take decades. For now, and for the foreseeable future, what the Fed does in Washington remains one of the most powerful external forces shaping India's economic destiny.

13. The Indian Investor's Action Plan

Understanding the Fed's impact is intellectually satisfying. But what should an Indian investor actually do with this knowledge?

Monitor the Fed Cycle, Not Just One Move

Single rate decisions matter less than the overall cycle direction. A rate-hiking cycle (Fed raising rates over multiple meetings) signals sustained dollar strength, capital outflow risk, and rupee pressure. A rate-cutting cycle signals the opposite. Position your portfolio accordingly — not reactively to each meeting, but strategically to the cycle direction.

Watch the Dollar Index (DXY)

The DXY measures the dollar's strength against a basket of major currencies. A rising DXY generally correlates with rupee weakness and FPI outflows from India. A falling DXY correlates with rupee strength and capital inflows. Track it alongside Fed meetings as a forward indicator.

Diversify Across Interest-Rate Sensitivities

During Fed hiking cycles, overweight IT and pharma exporters (which benefit from rupee weakness) and underweight rate-sensitive sectors (real estate, banking). During Fed easing cycles, reverse the allocation — banking, real estate, and consumer discretionary tend to outperform.

Consider Dollar-Denominated Assets

For Indian investors, holding a portion of wealth in dollar-denominated assets — whether US equity index funds, international ETFs, or sovereign gold bonds — provides a natural hedge against rupee depreciation during Fed hiking cycles. When the rupee falls, those dollar assets appreciate in rupee terms.

Don't React Emotionally to Every FOMC Statement

Markets often overreact to Fed communications. A "hawkish pause" — where the Fed holds rates but signals future hikes — can trigger sharp selloffs. But if India's underlying fundamentals (GDP growth, earnings, current account) are sound, these moves often create buying opportunities. The long-term Indian growth story is not derailed by US rate cycles; it is temporarily affected by them.

Stay Informed on the Rupee and Crude

Two numbers to track constantly: the USD/INR exchange rate and Brent crude oil price. Both are direct transmission channels of Fed policy into India's economy. A sharp rupee depreciation or crude oil spike — often triggered or amplified by Fed moves — is an early warning signal to reassess portfolio risk.

"In today's interconnected world, a butterfly flapping its wings in the United States can create an economic tornado in India." — A metaphor now backed by decades of data

The US interest rate is not a foreign curiosity. It is a number that touches the price of the fuel in your car, the EMI on your home loan, the returns in your equity portfolio, and the currency in which your savings are stored. The Federal Reserve was created to serve America's economy — but in a world bound together by dollar trade, petrodollar energy flows, and integrated capital markets, it effectively sets monetary conditions for much of the planet.

India has built remarkable economic resilience over the past three decades. Its domestic growth drivers — a young population, rising consumption, digital infrastructure, manufacturing ambitions — are real and powerful. But resilience is not immunity. The global financial system, wired through the dollar, ensures that Washington's decisions always find their way to Dalal Street.

The investor who understands this is not at the mercy of it. They are prepared for it.

For educational purposes only. This article does not constitute investment advice. Always consult a registered financial adviser before making investment decisions.