4 Optical Fiber Stocks to Watch as AI Pushes Market Beyond $100 Billion

There is a quiet but powerful revolution happening beneath the surface of the global AI boom, and it runs on glass. While most investors are chasing semiconductors, GPUs, and cloud platforms, the real backbone of the AI era is optical fiber. Every data center being built for AI needs thousands of kilometers of it. Every 5G tower, every broadband connection, every hyperscale facility put up by Meta, Microsoft, or Google, all of it depends on optical fiber. And that demand is creating a serious, multi-year investment opportunity right here in India.

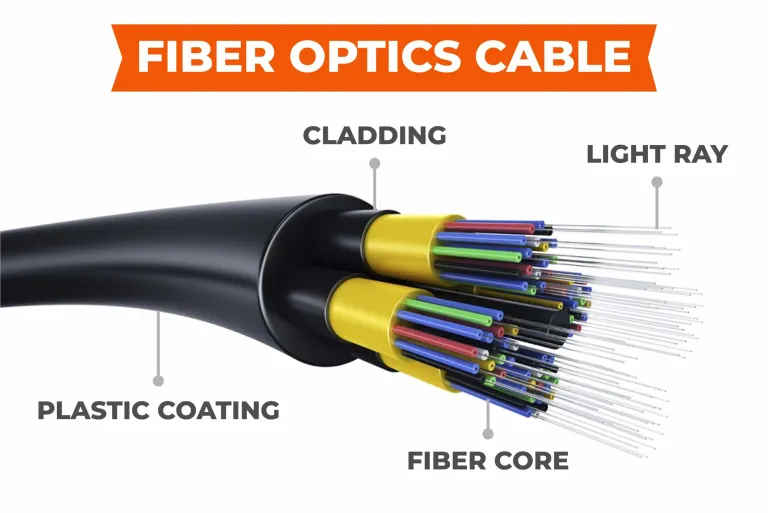

What is Optical Fiber and Why Does It Matter?

Optical fiber is a thin strand of glass or plastic that carries data as pulses of light. Unlike traditional copper cables that carry electrical signals, optical fibers transmit information over much longer distances and with far less signal loss. A single fiber strand, thinner than a human hair, can support multi-terabit capacity in advanced commercial deployments, making it the undisputed foundation of modern digital infrastructure. As of 2024, global fiber optic deployments surpassed 4.8 million kilometers, driven by unprecedented internet usage and the rapid expansion of 5G infrastructure. Over 5.4 billion individuals now use the internet, with more than 70% accessing it through broadband connections underpinned by fiber optics.

Modern hyperscale and cloud data centers already use 80–90% fiber optics, a figure that will only rise. Telecom and internet infrastructure account for the bulk of global fiber demand today, but the fastest-growing use case is now something categorically different: AI data centers. AI has evolved from a futuristic concept to a ubiquitous technology, and to cope with the exploding demand for AI, many new data centers are needed, all of which must be connected via cables, with optical fiber being the superior choice for achieving the highest transmission speeds, particularly across long distances.

Why Demand is Surging

For most of the last decade, optical fiber demand grew steadily, driven primarily by telecom and broadband expansion. That dynamic is now shifting rapidly with the rise of AI. The global optical fiber cable market is estimated at around $80–85 billion in 2025 and is expected to grow to over $110 billion by 2030, implying a steady CAGR of ~6–7%.

At the same time, the broader fiber optics ecosystem—including components and connectivity hardware—is expanding even faster, with the global market projected to grow from ~$35–37 billion in 2025 to nearly $58–60 billion by 2030, at a CAGR close to 9–10%.

India, while smaller in absolute size, is growing significantly faster. The domestic optical fiber cable market is estimated at ~$0.5–0.9 billion in 2025 and is expected to more than double over the next decade, with growth rates ranging between 10% and 14% CAGR, driven by 5G rollout, BharatNet, and data center expansion.

The top four US hyperscalers, Amazon, Google, Meta, and Microsoft, increased their data center capital expenditure by 76% in 2025, with combined spending crossing $420 billion. Amazon alone spent $125 billion, up from $83 billion in 2024. Microsoft spent $80 billion, Google $75 billion, and Meta $65 billion. And the pace is not slowing. According to CreditSights, the top five hyperscalers are projected to spend approximately $602 billion in 2026, a further 36% year-on-year increase, with roughly 75% of that, or about $450 billion, directly tied to AI infrastructure.

All of this spending flows directly into fiber demand. The reason is structural. According to Corning, one of the world's largest fiber manufacturers, generative AI-enabled data centers currently require over 10 times more optical fiber than traditional data center networks. STL's own CEO goes further: Rahul Puri, CEO of the Optical Networking Business at STL, has stated that AI-focused data centers require about 36 times more fiber than traditional CPU-based racks, to handle the massive data volumes and high-speed connectivity required by GPU clusters. He also projects that the US alone will need to add 213.3 million more fiber miles by 2029, more than doubling its current amount from 159.6 million fiber miles to 372.9 million miles.

The secondary market data reinforces this. Between 2023 and 2024, metro dark fiber purchases rose by 268%, while long-haul dark fiber purchases grew by 53%. Total bandwidth purchases more than doubled during 2020–2024, growing by nearly 133% to reach 42.4 terabits. Zayo reported more than $1 billion in AI-related long-haul network deals in 2024 alone, with another $3 billion in the pipeline.

Geographically, the demand is global. China remains the top country in optical fiber deployment, with over 1.2 million kilometers installed in 2023. Emerging markets such as India, Vietnam, and Brazil reported a 30–45% year-on-year increase in fiber deployments. Governments worldwide are not sitting still either — India's BharatNet targets over 2 million kilometers of rural fiber, the US BEAD program has allocated $42.45 billion to underserved communities, and the EU's Connecting Europe Facility has committed over €3 billion to cross-border fiber connectivity.

The supply-side constraint is equally important to understand. Optical fiber preform — the critical raw material used to manufacture fiber — takes 18 to 24 months to meaningfully scale up production. This structural lag between surging demand and constrained supply is already pushing fiber prices higher globally. As GPU clusters scale toward 50,000-plus nodes, optical infrastructure is becoming a strategic resource, explaining the sharp rise in fiber pricing entering 2026. For Indian manufacturers sitting on existing capacity and actively expanding, this is a textbook pricing tailwind — and four companies are positioned right at the center of it.

4 Stocks to Keep Under Your Radar

1. Sterlite Technologies (STL)

STL is India's largest optical fiber and optical fiber cable manufacturer, and one of the largest globally outside China. The company is named among the world's key fiber manufacturers alongside Corning, Prysmian, Sumitomo Electric, and Fujikura, a peer group that tells you exactly the league STL is competing in. Its manufacturing presence spans India, Italy, and the United States, with its US plant BABA-compliant under America's Infrastructure Investment and Jobs Act, a critical advantage that shuts out Chinese competitors from a significant portion of US government-linked contracts.

STL is methodically positioning itself as an AI-ready digital infrastructure player, with a growing focus on hyperscale data center customers in the US and Europe, where order realisations are meaningfully higher than domestic contracts. The company is also investing in next-generation fiber technologies, including Hollow Core Fiber, which guides light through air instead of glass, cutting propagation delay and reducing end-to-end latency by approximately 30%, alongside Multi-Core Fiber and G.654.E ultra-low-loss fiber, all specifically designed for the latency and bandwidth demands of AI infrastructure.

2. HFCL Limited

HFCL is a leading Indian manufacturer of optical fiber cables and broadband equipment, with a product portfolio spanning aerial, armored, FTTx, micro, and underground cable types, covering telecom, defense, and data center applications. What makes HFCL particularly interesting right now is the scale and pace of its capacity expansion, happening at exactly the moment global fiber demand is peaking.

The company has doubled its optical fiber manufacturing capacity from 14 million fiber-kilometres per annum to 28 million fkm, with further expansion planned to 33.9 million fkm by December 2026. Its optical fiber cable capacity is simultaneously being raised from 30.5 million to 42.36 million fkm by June 2026. These are not incremental adjustments; they represent a company placing a large, deliberate bet on the fiber supercycle. HFCL has also set up a manufacturing unit in Poland for optical fiber cables with an output capacity of 3.25 million fiber-km to meet emerging demand, a clear sign of its global ambitions. The company has signed a five-year supply agreement with a global multinational for high-fibre-count cables, with exports growing rapidly as a share of total revenue.

3. Tejas Networks

Tejas Networks, backed by Tata Sons, occupies a distinct position in the fiber ecosystem — it does not manufacture fiber, it builds the optical and data networking equipment that runs on it. The company supplies optical transport systems, IP/MPLS routers, and GPON equipment to telecom operators, ISPs, utilities, and governments across 75+ countries.

Tejas is explicitly targeting the AI data center opportunity. In a recent Censuswide survey of over 1,300 data center decision-makers worldwide, respondents predicted that data center interconnect bandwidth will grow by six times by end of the decade, with 67% planning to enlist managed optical fiber services to link multiple data centers, 43% of which will be dedicated to AI. Tejas is positioning itself squarely to serve this need, with next-generation WDM optical transport platforms purpose-built for terabit-scale data center interconnections. The company is also a leading supplier for BharatNet Phase III, India's rural broadband backbone — giving it a strong domestic order pipeline alongside its international ambitions. It is a higher-risk, longer-horizon bet, but with significant operating leverage if its strategy plays out.

4. Birla Cable

Birla Cable, part of the M.P. Birla Group, is the quietest name on this list — a pure-play optical fiber cable manufacturer operating out of Rewa, Madhya Pradesh, with a product portfolio spanning ADSS cables, armored cables, FTTx, micro-duct cables, and specialty designs for telecom, railways, and defense applications.

The company recently announced a capacity expansion, increasing its optical fiber cable capacity from 81,848 to 96,848 cable kilometres — an 18% addition — backed by a ₹17 crore investment. The stated rationale directly echoes the global trend: rising demand and the need to cater to higher-speed fiber technologies. For investors, Birla Cable is a small-cap, higher-risk entry into the same structural theme. As fiber prices rise and industry-wide utilization rates climb, smaller manufacturers can benefit disproportionately from improved realisations — even without dramatic volume growth. At a much smaller base, meaningful percentage gains become achievable faster.

The Bigger Picture

The optical fiber boom of 2026 is structurally different from the dot-com era fiber glut of the early 2000s. That build-out was speculative — driven by projections of demand that had not yet materialised. Today's build-out is being funded by the world's most profitable companies, who have raised record levels of debt specifically to finance AI infrastructure — with the Big Four hyperscalers already spending 94% of operating cash flow on their AI build-outs. This is not speculation. It is committed capital, already being deployed.

For India, this is a moment to pay attention to. The country is simultaneously among the fastest-growing fiber deployment markets globally, a rapidly expanding export hub for fiber cables, and home to companies winning contracts from some of the world's largest technology buyers. The opportunity is real, the tailwind is structural, and four Indian companies are sitting right at the center of it.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Please consult a SEBI-registered financial advisor before making investment decisions. Stock market investments are subject to market risks.