Planning to Buy Term Insurance? Here’s Everything You Need to Know

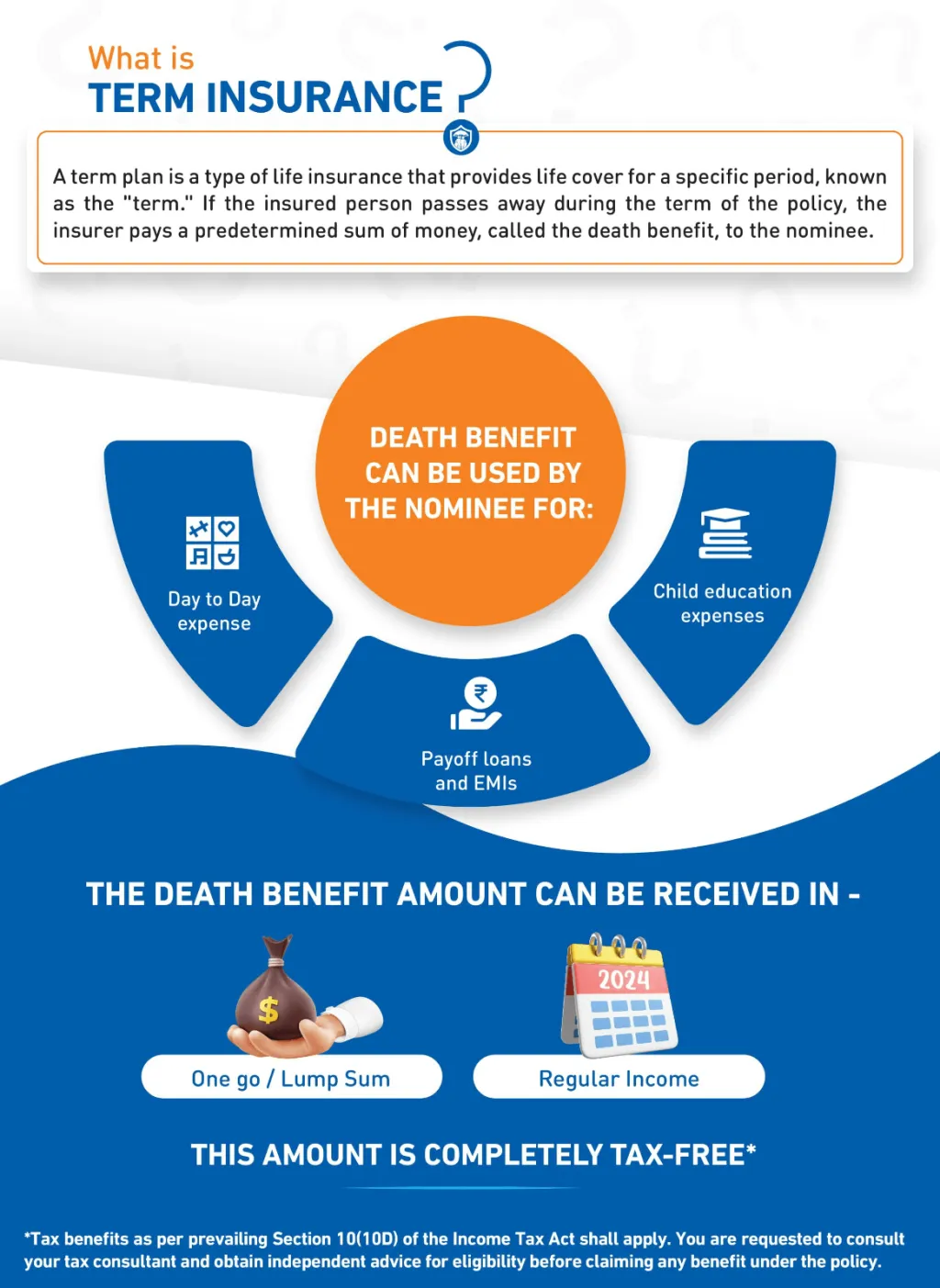

What Is Term Insurance?

Term insurance is the simplest, purest form of life insurance you can buy. In exchange for regular premium payments, it provides your family with a financial safety net for a defined number of years. If you pass away while the policy is active, your nominated beneficiary receives a lump sum — the death benefit — which can cover everything from daily household expenses to children's education and outstanding loans.

Unlike investment-linked plans or endowment policies, term insurance carries no savings component. It exists for one purpose only: to protect the people who depend on you financially. Because of this stripped-down structure, the premiums are far more affordable than other life insurance products. A healthy 20-year-old non-smoker male, for instance, can secure a ₹1 crore life cover for roughly ₹19 per day.

If you survive the full policy term, a standard plan pays nothing back — the coverage simply ends. However, if you want your money returned, you can opt for a Term Insurance with Return of Premium (TROP) variant, where all premiums are refunded at maturity.

How Does Term Insurance Work?

Here's a simple walk-through using a real-life example.

Say Pranjal is a 25-year-old non-smoker who buys a ₹1 crore term plan for a 35-year tenure. He completes a health assessment, undergoes required medical tests, and begins paying his monthly premium.

Throughout the policy period, he simply keeps up with his payments. If Pranjal were to pass away during the policy term, his wife or his nominated beneficiary would receive the full ₹1 crore as a tax-free death benefit. If he outlives the policy, the coverage ends when he turns 60. Had he opted for the return of premium variant, he would have got all his paid premiums back at that point. That's the core mechanic: pay premiums, stay covered, protect your family.

Why Should You Buy Term Insurance in 2026?

1. Financial protection for your dependents: If you are the primary earner in your family, your income is essentially the engine that keeps everything running, such as household expenses, school fees, EMIs, and medical costs. A term plan replaces that income for your family in your absence.

2. Protection against debt: Home loans, car loans, and personal debt don't disappear when you do. The death benefit from a term plan ensures your family isn't left scrambling to repay outstanding liabilities.

3. Coping with new-age lifestyle risks: India recorded an average of 474 road accident deaths per day in 2023. Cancer claimed over 8.89 lakh lives in 2022. These aren't distant statistics; they're reminders that life is unpredictable, and financial preparation is the only rational response.

4. High coverage at very affordable premiums: Because term insurance offers pure protection with no investment element, premiums are kept low. A ₹1 crore cover can cost as little as ₹19/day for a young, healthy individual.

5. Riders for broader protection: You can enhance your base term plan with add-ons like critical illness cover, accidental death benefit, or waiver of premium — giving you a more rounded financial safety net.

6. Tax savings: Premiums paid qualify for deductions under Section 80C (up to ₹1.5 lakh annually), and the death benefit received by your nominee is fully tax-free under Section 10(10D). If you add health-related riders, you can additionally claim deductions under Section 80D.

7. Preparing for lifestyle disease risks: Heart attack cases in India rose by 12.5% between 2021 and 2022. Diabetes affects 100 million Indians. A term plan, especially with a critical illness rider, ensures your family is financially protected even if a serious illness strikes.

8. Zero GST benefit As of September 22, 2025, individual term insurance premiums are fully exempt from GST, making protection even more affordable.

Real-Life Scenarios: Term Insurance at Different Life Stages

Rahul, 27 — A new professional: Starting his first job in Mumbai, Mridul finds managing expenses tight. He opts for a term plan that offers a 15% first-year discount for salaried employees, a premium break of up to 12 months in case of job loss, and an option to increase life cover by up to 200% on major milestones like marriage or having a child. His family is now protected as he builds his career.

Key Benefits of Term Insurance

Tax benefits — deductions under Sections 80C, 80D, and 10 (10D)

High life cover at low cost — ₹1 crore coverage for under ₹20/day (for some insurers)

Income replacement — the death benefit substitutes for lost earnings

Loan protection — ensures EMIs and outstanding debt are covered

Long-term peace of mind — coverage available up to 85 years of age

Optional return of premium — get all your premiums back if you outlive the policy

Rider flexibility — add coverage for critical illness, accidental death, disability, and more

Key Features of Term Insurance

Pure protection: No savings or investment component, every rupee of premium goes towards providing life cover.

Affordable, fixed premiums: Premiums are locked in at the time of purchase and don't change through the policy term.

Flexible coverage amount: You can determine the right sum assured using the D.I.M.E. formula, adding up your Debt, Income replacement needs, Mortgage, and Education costs for dependents. For example: ₹5L in loans + ₹15L annual income + ₹1Cr home loan + ₹25L education costs = ₹1.45 Cr, so a ₹1.5 Cr cover makes sense.

Choice of policy term: You can opt for a term as short as 5 years or as long as coverage till age 85, depending on your financial responsibilities.

Flexible payout options: Choose a lump sum, monthly income, increasing monthly income, or a combination.

Rider add-ons:

Critical illness rider — upfront payout on diagnosis of covered illnesses

Accidental death benefit rider — additional payout on top of the base death benefit

Waiver of premium rider — future premiums waived if you become critically ill or permanently disabled

Maturity benefits: Standard plans offer none. TROP variants return all premiums at policy maturity.

Tax savings: Deductions under Sections 80C, 80D, and 10(10D) of the Income Tax Act, 1961.

Who Should Buy Term Insurance?

Parents with young children: Education costs in India are rising sharply — school fees have increased 50–80% between 2022 and 2025 for many families. A term plan ensures children's education is secured regardless of what happens to you.

Newly married couples: A term plan protects your spouse from financial hardship and covers shared goals like home loan repayment.

Individuals supporting elderly parents or siblings: If you are the financial pillar for older or younger dependents, a term plan gives them a cushion in your absence.

Primary earners: Your income keeps the household running. The death benefit replaces that income stream if you're no longer around.

Home loan borrowers: Home EMIs are a significant monthly commitment. A term plan ensures the family doesn't lose the home in your absence.

Young working professionals: Buying early locks in lower premiums. A healthy 25-year-old pays ₹8,071 annually for a ₹1 crore cover, and by 35, that rises by ~38% to ₹13,031 per annum.

Working women: Women who contribute to household income have the same financial responsibilities as male breadwinners. Term insurance for women also comes with a premium advantage; women typically pay about 18% less than men at the same age.

Homemakers: Though they may not earn directly, homemakers contribute significantly to household functioning. Their absence creates real financial costs, such as childcare and household management, that a term plan can help offset.

Taxpayers: Premium deductions can save up to ₹46,800 annually under Section 80C (at 30% tax bracket), plus additional savings under 80D for health-related riders.

Self-employed and entrepreneurs: Unlike salaried employees, they have no employer-provided group cover, no provident fund, and often carry business debt. Term insurance is even more critical for this segment.

NRIs: India's competitive insurance market offers NRIs affordable premiums, global coverage, and an 18% GST waiver on premiums paid from NRE accounts.

Senior citizens: Even in retirement, term insurance can protect a dependent spouse, cover outstanding loans, or help leave a financial legacy for children.

When Should You Buy Term Insurance?

The short answer: as early as possible. Premiums increase with age because mortality risk increases. Here's a snapshot of how much more expensive waiting costs:

Age at Purchase | Annual Premium (₹1 Cr cover, till 60) | Years of Coverage |

|---|---|---|

25 years | ₹9,025 | 35 years |

30 years | ₹10,294 | 30 years |

35 years | ₹12,658 | 25 years |

40 years | ₹17,002 | 20 years |

45 years | ₹21,691 | 15 years |

The five key life events that should prompt a term insurance purchase are: when you start earning, when you get married, when you become a parent, when you take on a significant loan, and when you move to a new country.

Types of Term Insurance Plans in India (2026)

1. Level Term Plan — Sum assured stays constant throughout the policy tenure.

2. Annually Renewable Term — Policy renews every year; premiums increase annually as you age.

3. Decreasing Term Plan — The death benefit reduces over time. Typically taken alongside a home loan, as the outstanding principal also reduces.

4. Increasing Term Plan — The death benefit grows annually to account for inflation.

5. Convertible Term Plan — Gives you the option to convert your term policy into a permanent life insurance plan during a defined conversion window.

6. Joint Life Term Plan — Covers two lives (usually spouses) under a single policy, with either shared or separate cover amounts.

7. Term Insurance with Return of Premium (TROP) — All premiums are refunded at the end of the policy term if the policyholder survives.

Term Insurance vs. Whole Life Insurance

Feature | Term Insurance | Whole Life Insurance |

|---|---|---|

Coverage period | Defined term (up to age 85) | Till age 100 |

Purpose | Income and debt protection during working years | Long-term financial legacy |

Premiums | Lower | Higher |

Investment component | None | None |

Survival benefit | TROP variant only | No payout until death |

Loan against policy | Not available | Not available |

Conversion option | Some plans offer it | Not applicable |

How to Choose the Right Term Insurance Plan

Step 1 — Assess your family's financial needs: Calculate daily living costs, outstanding loans, children's future education, and long-term goals. The sum assured should be enough to cover all of these.

Step 2 — Check the Claim Settlement Ratio (CSR): This tells you what percentage of claims the insurer has settled in a given year. A consistently high CSR signals reliability. Step 3 — Evaluate customer experience: Look at reviews, responsiveness, and the quality of service during both policy servicing and claim settlement.

Step 4 — Check the Solvency Ratio: Insurers with a solvency ratio above 1.5 (150%) have adequate reserves to honour long-term claims.

Step 5 — Compare benefit structures: Look at what the plan covers beyond basic death benefit — maturity options, payout flexibility, and premium break provisions.

Step 6 — Choose relevant riders: Only add riders that address real risks in your life — don't over-insure with unnecessary add-ons.

Step 7 — Decide on a payout structure: A lump sum suits situations like home loan repayment; monthly income payouts work better for ongoing living expenses.

Step 8 — Buy online: Online plans often come cheaper due to fewer intermediary costs, and also offer greater transparency and convenience.

Step 9 — Understand the grace period: Typically 15 days for monthly payers and 30 days for annual payers — a buffer if you miss a due date.

Step 10 — Know the free look period: You have 30 days from receiving policy documents to review and cancel for a refund (minus nominal charges) if the plan doesn't meet your expectations.

Step 11 — Check for Smart Exit Benefit: Some plans allow you to exit early and recover a portion or all of the premiums paid, depending on conditions.

How Does a Term Plan Secure Your Family's Future?

Education continuity — school fees and college costs don't stop; the death benefit ensures they're covered

Funeral and end-of-life expenses — these are often unexpectedly high and can burden a grieving family

Business continuity — if you're a business owner, the payout helps cover operational costs during a transition

Estate planning — helps transfer assets to heirs without forcing asset sales to cover estate costs

Debt repayment — ensures loans don't become a burden for surviving family members

Income replacement — provides a financial substitute for the income that is lost

Death benefit — the core function: a lump sum that can be deployed across all of the above

How Are Term Insurance Premiums Calculated?

Several factors determine your premium:

Age — younger buyers pay less; mortality risk rises with age.

Gender — women statistically live longer and typically pay about 18% less than men.

Health and medical history — pre-existing conditions, family history of illness, past surgeries, all affect the risk profile.

Lifestyle habits — smokers pay significantly more. A 30-year-old smoker pays nearly double the premium of a non-smoker for the same cover.

Profession — high-risk jobs (sailors, pilots, construction workers) attract higher premiums.

Riders chosen — each add-on increases the premium modestly.

Sum assured — a higher cover means a higher premium.

Policy term — longer coverage periods generally attract higher premiums.

Premium paying term — choosing to pay for 20 years instead of 30 for the same policy tenure increases your annual outgo by roughly 22%.

The Impact of Age on Premiums — A Snapshot

Age | Non-Smoker Premium | Smoker Premium | Extra Cost of Smoking |

|---|---|---|---|

25 | ₹8,034/yr | ₹14,060/yr | ₹6,026/yr = ₹1.8L over 30 yrs |

30 | ₹10,294/yr | ₹18,015/yr | ₹7,721/yr = ₹2.3L over 30 yrs |

35 | ₹14,440/yr | ₹22,152/yr | ₹7,712/yr = ₹1.9L over 25 yrs |

40 | ₹17,002/yr | ₹29,753/yr | ₹12,751/yr = ₹2.6L over 20 yrs |

Gender and Premiums

Age | Male (Non-smoker) | Female (Non-smoker) | Female Savings |

|---|---|---|---|

25 | ₹8,034/yr | ₹6,829/yr | ₹36,150 over 30 years |

30 | ₹10,294/yr | ₹8,750/yr | ₹46,320 over 30 years |

35 | ₹12,658/yr | ₹10,760/yr | ₹22,776 over 25 years |

40 | ₹17,002/yr | ₹14,451/yr | ₹30,612 over 20 years |

How Much Cover Do You Actually Need?

There are several methods to estimate the right sum assured:

Expense replacement: Total all your current and future expenses, then subtract your existing savings, investments, and any existing life cover.

Income replacement: Multiply your annual income by the number of years until your youngest dependent becomes financially independent.

10–15x annual income rule: A straightforward thumb rule — take 10 to 15 times your annual income as the minimum cover.

D.I.M.E. formula: Add up Debt + Income (replacement) + Mortgage + Education costs. Example: ₹5L + ₹15L + ₹1Cr + ₹25L = ₹1.45 Cr; round up to ₹1.5 Cr.

Human Life Value (HLV): A more comprehensive actuarial approach that factors in future earnings potential, inflation, and expected liabilities.

How to Choose the Right Policy Duration

The ideal term depends on several personal factors:

Financial dependence of children — the cover should last at least until they're economically self-sufficient

Loan repayment timelines — if your home loan runs for 25 years, your cover should extend at least as long

Your planned retirement age — post-retirement, income is typically replaced by savings; the cover can wind down

Your current age — the younger you are, the longer the tenure you may need

Spouse's financial dependency — if your spouse is not independently earning, the policy should outlast your expected working years

Overall financial dependency — parents, siblings, and other dependents all extend the horizon of financial responsibility

A common guideline for someone in their 30s is to take a 30-year policy, which takes them through to their 60s when most major financial obligations — loans, child education — are typically resolved.

Why Term Insurance Premiums Rise with Age

The core reason is rising mortality risk. As you grow older, the statistical probability of death within the policy term increases, which means the insurer is more likely to pay a claim. Additionally, older individuals are more prone to health conditions like diabetes, hypertension, and heart disease — all of which add to the risk profile. Finally, reinsurers (the companies that insure insurers) also charge more for older lives, and those costs trickle down to policyholders.

How to Reduce Your Term Insurance Premium

Buy young — premiums are lowest when you're young and healthy. Delaying from age 25 to 35 can increase your annual premium by 35% or more.

Quit smoking — non-smokers pay roughly half of what smokers pay for the same coverage.

Manage your health — conditions like obesity, diabetes, and hypertension raise your risk profile and therefore your premium.

Choose the right sum assured — don't over-insure; use a calculator to determine the coverage you actually need.

Pick a tenure aligned with your needs — unnecessarily long tenures increase premiums.

Buy online — online purchases can attract discounts of up to 5% on first-year premiums with some insurers.

Payout Options in Term Insurance

1. Lump sum — the full death benefit is paid out in one go at the time of claim.

2. Monthly income — the benefit is distributed as a monthly payout to help the family manage ongoing expenses.

3. Increasing monthly income — like the monthly option, but the payout increases at a fixed percentage each year to account for inflation.

4. Lump sum + monthly income — a combination where part of the benefit is paid immediately, and the rest is spread over time.

Term Insurance Riders — Everything You Need to Know

Riders are optional add-ons that extend your base policy's coverage for a small additional premium. Think of them as top-up packs on your insurance plan.

Critical illness rider — pays out a lump sum if you're diagnosed with any of the covered conditions (typically including heart attack, cancer, kidney failure, and others). This covers treatment costs and recovery expenses. For example, a woman with a ₹1 crore term plan and a ₹20 lakh critical illness rider would receive the ₹20 lakh upon a breast cancer diagnosis — and her base ₹1 crore term cover would continue unchanged.

Accidental death benefit rider — provides an additional payout over and above the base death benefit if death occurs due to an accident.

Waiver of premium rider — if you are diagnosed with a critical illness or become permanently disabled during the policy term, the insurer waives all future premium payments, but your policy continues in full force.

Accidental total and permanent disability rider — pays a sum assured if an accident results in permanent disability that affects your ability to earn.

Terminal illness rider — provides an advance payout if you are diagnosed with a terminal illness, helping cover treatment and other urgent needs.

Live well rider — a wellness-focused rider that combines a death benefit with benefits like OPD consultations and preventive health checkups.

Why riders matter: They enhance coverage without requiring you to buy separate policies. A ₹50 lakh base plan might cost ₹8,000 annually — adding a critical illness rider may raise it to only ₹9,000, delivering significantly broader protection. They're also eligible for additional tax deductions: health-related riders qualify under Section 80D, offering dual tax-saving benefits alongside the base plan's Section 80C deduction.

Why Buy Term Insurance Online?

Lower premiums — no agent commission means cheaper plans

Convenience — compare, customise, and pay from home

Transparency — full product details, exclusions, and terms are available directly on the insurer's website

Premium discounts — some insurers offer first-year discounts for online purchases

Easy premium calculation — built-in calculators let you compare scenarios instantly

Digital document submission — no need to physically submit papers

What Is and Isn't Covered in Term Insurance?

Covered:

Death due to terminal illness

Death due to medical conditions

Death due to natural calamities

Death due to accidents

Not covered:

Suicide within the first year of the policy

Claims arising from the misrepresentation of material information

Common Mistakes to Avoid

1. Buying late — every year you delay, the premium goes up. Start as soon as you have a steady income.

2. Under-insuring — don't pick a cover amount based on what's being sold to you. Calculate what your family actually needs.

3. Ignoring riders — critical illness and accidental death riders add substantial protection for a marginal increase in premium.

4. Providing inaccurate information — this is the single biggest reason for claim rejections. Always be fully transparent about your health, income, and lifestyle.

5. Choosing too short a tenure — your policy should last as long as your dependents rely on your income, not just until your next career milestone.

6. Not buying online — you miss out on discounts and the ease of comparison.

The Claim Process

Step 1 — Intimate the claim: Notify the insurer via their website, email, SMS, or customer care as soon as possible after the policyholder's death.

Step 2 — Documentation: Submit the required documents (death certificate, policy document, claimant's identity proof, bank details, and any medical or accident-related records).

Step 3 — Verification: The insurer verifies and may investigate the claim. This can take a few days to a few weeks.

Step 4 — Settlement: IRDAI mandates insurers to settle claims within 15 days of receipt of all documents. If further investigation is needed, the insurer has 45 days to make a decision.

How to Ensure Smooth Claim Settlement

Disclose everything accurately at the time of purchase — medical history, lifestyle habits, income, existing policies, and any previous rejections

Fill your own application form — don't rely on agents

Read the policy document carefully — understand exclusions and waiting periods

Appoint the right nominee — keep their details current; appoint a guardian if the nominee is a minor

Pay premiums on time — or use the grace period if needed; set up auto-debit as a safeguard

Inform your nominee about the policy — they should know where the documents are and how to initiate a claim

Key Takeaways

Term insurance is one of the most important financial decisions you can make — not for yourself, but for everyone who depends on you. It is affordable, straightforward, and extraordinarily effective at its core purpose: making sure the people you love are financially protected even after you are gone. But remember that you should buy early, buy adequate cover, be honest in your application, choose relevant riders, and keep your nominee informed. That's the entire playbook, and it can make all the difference when it matters most.