4 Govt Schemes Offering Upto ₹50L Funding Without Collateral in India

India is home to one of the fastest-growing startup ecosystems in the world. With over 6 crore registered startups contributing more than 30% of the country's GDP, entrepreneurship is no longer a path less taken — it is a movement. Yet, for most first-generation founders, the single biggest wall between a great idea and a real business is funding.

Banks ask for collateral you don't have. Investors want the traction you haven't built yet. And bootstrapping only takes you so far.

What many founders don't realise is that the Government of India has quietly built a powerful safety net of schemes specifically designed to solve this problem — offering loans without collateral, grants without equity dilution, and credit guarantees that make banks far more willing to say yes. These are not obscure programs buried in government paperwork. They are active, well-funded, and accessible to you right now.

Here are the four most impactful government-backed schemes every Indian startup founder should know about in 2025 and 2026.

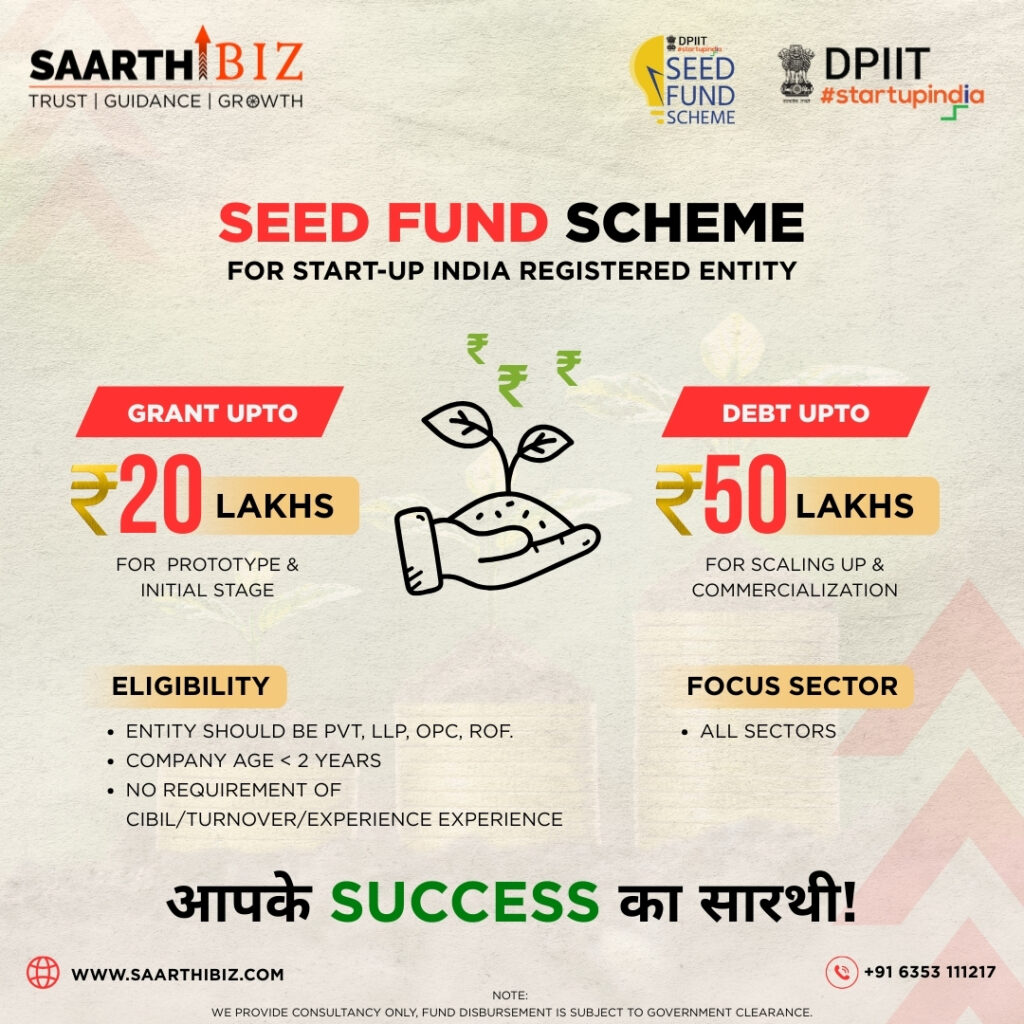

1. Startup India Seed Fund Scheme (SISFS)

If you are at the idea stage or early prototype stage, this is probably the most relevant scheme for you. The Startup India Seed Fund Scheme was launched by the Department for Promotion of Industry and Internal Trade (DPIIT) with a total sanctioned budget of Rs 945 crore, and it has already disbursed funds to over 3,600 startups since 2021.

The scheme is designed to bridge the gap between having a concept and having something investable. Early-stage startups often struggle to secure capital from banks or private investors precisely because they do not yet have a market-tested product. SISFS fills that gap by providing structured financial assistance before you reach that stage.

What you get is genuinely substantial. Grants of up to Rs 20 lakhs are available for proof of concept, prototype development, or product trials. Beyond that, investment of up to Rs 50 lakhs is available via debt or convertible debentures for market entry or scaling. Critically, there is no collateral requirement and no personal guarantee needed. The scheme also comes with full incubation support including mentoring, infrastructure access, compliance help, and investor connections — and no fees are charged from the startup for fund disbursement.

The scheme is disbursed through DPIIT-approved incubators spread across India, which ensures regional accessibility and transparency. To be eligible, your startup must be DPIIT-recognised, incorporated within two years of application, have an innovative and scalable product or service, and have Indian promoters holding at least 51% equity.

Notable startups that have already benefited include Aloe Ecell in biotech, TechpromIot in IoT, and Biovantis Healthcare in healthtech. If your startup is in any sector — the scheme is industry-agnostic — this should be your first port of call.

How to apply: Register on the Startup India portal, obtain your DPIIT recognition, and then apply through an eligible incubator listed on the SISFS portal.

2. Pradhan Mantri MUDRA Yojana (PMMY)

Launched on April 5, 2015, the Pradhan Mantri MUDRA Yojana is one of the most accessible and widely used government loan schemes in India. It provides collateral-free loans to individuals running non-corporate, non-agricultural small enterprises, and as of 2025, over Rs 31.85 lakh crore has been disbursed under this scheme, empowering millions of micro and small businesses across the country.

What makes MUDRA stand out is its simplicity and reach. Loans are available through public sector banks, regional rural banks, NBFCs, and microfinance institutions. The process requires minimal paperwork and caters to businesses in services, manufacturing, and trading sectors across both urban and rural India.

The scheme is structured into three tiers based on your stage of business:

Shishu covers loans up to Rs 50,000 and is designed for startups at the idea or very early stage. Kishor covers loans from Rs 50,001 to Rs 5 lakhs for businesses that have already started and need working capital to grow. Tarun covers loans from Rs 5 lakhs to Rs 20 lakhs for more established micro enterprises looking to scale further.

No security or collateral is required for loans up to Rs 10 lakhs, and the scheme offers flexible repayment terms of up to 5 to 7 years. Interest rates are not fixed centrally but are kept reasonable and affordable by the lending institutions, making it a practical choice for founders who need working capital without giving up equity or pledging assets.

If you are running a small service business, a local manufacturing unit, or a trading venture and need initial capital to get moving, PMMY is arguably the most straightforward path to formal credit in India today.

How to apply: Visit any public sector bank, regional rural bank, NBFC, or microfinance institution. You can also apply online through the Udyamimitra portal managed by SIDBI.

3. Credit Guarantee Scheme for Startups (CGSS)

For growth-stage startups that need larger loans but are struggling because banks want collateral they cannot provide, the Credit Guarantee Scheme for Startups is a game-changer. Launched by the Government of India specifically for DPIIT-recognised startups, CGSS offers credit guarantees on loans provided by scheduled commercial banks, NBFCs, and SEBI-registered Alternative Investment Funds.

The way it works is elegant. Instead of you having to pledge property or assets, the government acts as your guarantor. If you default, the Credit Guarantee Fund Trust for Startups covers a predefined percentage of the loss for the lender. This dramatically reduces the risk for banks and makes them far more willing to extend credit to startups that would otherwise be turned away.

The guarantee cover goes up to Rs 10 crore per startup, and the guarantee can be transaction-based or umbrella-based, depending on the lending institution's preference. Loans under this scheme come without any collateral requirement, making it one of the most powerful tools for startups that have moved past the seed stage but still lack the hard assets that traditional lenders demand.

CGSS is particularly impactful for deep tech, SaaS, and manufacturing startups where capital requirements are high but physical assets are limited. If you are at a stage where you need Rs 2 crore to Rs 10 crore to scale and banks have been reluctant, this scheme is precisely the intervention you need.

How to apply: Approach a scheduled commercial bank or NBFC that is a Member Institution under CGSS, present your DPIIT recognition and business financials, and request a loan covered under the scheme.

4. Stand-Up India Scheme

The Stand-Up India Scheme holds a distinct place in India's startup funding landscape because it targets a group that has historically been underserved by formal credit systems — women entrepreneurs and founders from Scheduled Caste and Scheduled Tribe communities.

Introduced by the Department of Financial Services, this scheme facilitates bank loans between Rs 10 lakhs and Rs 1 crore specifically for setting up new Greenfield enterprises in manufacturing, services, or trading sectors. The loans are composite in nature, covering both term loan and working capital requirements. The repayment tenure extends up to 7 years with a maximum moratorium period of 18 months, giving early-stage founders the breathing room they need before repayments kick in.

Crucially, no collateral is required. Coverage is provided under the Credit Guarantee Scheme, which means the lending risk is absorbed through the government guarantee mechanism rather than your personal assets.

The scheme also goes beyond just money. Comprehensive handholding support is available for business planning and execution, making it especially valuable for first-time entrepreneurs who may not have an established network of advisors or mentors. The borrower must not be in default to any bank or financial institution, and in the case of non-individual enterprises, at least 51% of shareholding and controlling stake must be held by either an SC/ST or a woman entrepreneur.

What this scheme recognises is a reality that data has consistently shown: when you remove financial barriers for women and underrepresented communities, the quality and resilience of the businesses they build is remarkable. If you fall into this category and have been putting off formalising your business because of capital constraints, Stand-Up India is specifically built for you.

How to apply: Approach any scheduled commercial bank directly. You can also use the Stand-Up India portal at standupmitra.in, which connects applicants with banks and provides handholding support throughout the process.

How to Make the Most of These Schemes

A few practical things worth knowing before you apply to any of these.

First, DPIIT recognition is your master key. Many of the most powerful schemes — SISFS, CGSS, and several tax benefits — require you to be a DPIIT-recognised startup. Getting this recognition is free, done entirely online through the Startup India portal, and opens up a wide ecosystem of support beyond just these four schemes. Do this first.

Second, these schemes are not mutually exclusive. A startup can, for example, be DPIIT-recognised and benefit from SISFS for early seed support, while simultaneously having its bank loan backed by CGSS as it scales. Think of them as layers of support across your growth journey rather than a single choice.

Third, documentation matters more than most founders expect. Clean financial records, a clear business plan, and proper KYC documents are the difference between approval and rejection. Start maintaining proper books from day one — not just for these schemes, but because it builds the credibility that all future funding, private or public, will depend on.

India's government has put real money behind its stated commitment to building a startup ecosystem. The schemes outlined here are not aspirational policies — they are active programs with significant disbursement histories and continued government backing going into 2026. The only thing standing between you and this capital is knowing it exists and taking the steps to apply.

Your idea deserves a real chance. These schemes exist to make sure funding isn't what stops it.